Budgetary Control System

Budgetary control system

Budget is a financial and/or quantitative statement prepared and approved prior to a period of time, to the policy to be pursued during that period for the purpose of attaining a given objective.

Budgetary control is the establishment of the budget relating to the responsibilities of executives to the requirements of the organisation, and the continuous comparison of actual with budgeted results. The advantages of budgetary control are –

(1) combines the ideas of different levels of management in the preparation of the budget;

(2) coordinates all the activities of a business in order to centralize control but decentralize responsibility onto each manager involved;

(3) plans and controls income and expenditure so as to achieve the highest profitability acts as a guide for management decisions;

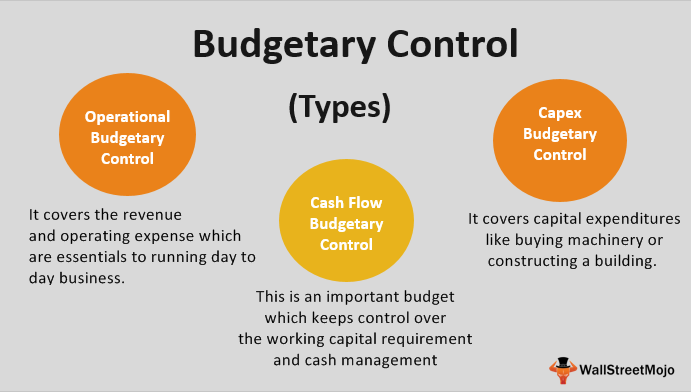

(4) ensures sufficient working capital and other resources for the efficient operation of the business;

(5) directs capital expenditure in the most profitable direction;

(6) reduces wastes and losses to a minimum and thus ensures an increase in productivity as regards men, machines and materials;

(7) provides a yardstick against which actual results can be compared; and

(8) shows management where effort is needed to remedy the situation without any delay.

Adequacy of Budgetary Control System:

In the area of planning:

1. Where it covers all interrelated functions like production, sales, purchasing, and finance.

2. Whether it determines the linkage between budget centers and responsibility centers.

3. Whether it establishes definite goals and limits for these functions well in advance. The system must answer questions such as “what they are expected to operate?” What will be the financial requirement for the functional areas? What would be the potential problems in the key areas?

4. Whether there are imbalances in the fixation of performance levels of functional budgets in relation to sales budgets.

5. Whether a budget monitoring cell exists for operating the system in the right perspective.

In the area of Coordination:

1. Whether the Budget monitoring committee holds the meetings regularly with a view to ensuring performance evaluation.

2. Whether it helps to prevent waste that results in duplicate or gross purpose activities.

3. Whether it reveals timelines in the process of preparation and approval of all functional Budgets and Master Budgets.

In the area of Control:

1. Whether a system exists for measuring, comparing and qualifying the results of all functional areas;

2. Whether the Budget incorporates a degree of flexibility with a provision of its periodical review;

3. Whether the various reports are issued in time and appropriate corrective action is taken on their variances.

Buy Classes: https://www.conceptonlineclasses.com/course/costaudit-pdhardbook-jun2019

#BudgetaryControlSystem

.jpg)

.png)

.png)

.png)

.png)

.png)

Top Reviews

Introduction to Statistics for CA Foundation

Introduction to Statistics for CA Foundation Business Mathematics, Logical Reasoning and Statistics is designed as per latest CA Foundation syllabus for Paper 3 to provide a firm grounding in the principles, techniques and practice. The book adopts self-study approach and has been written in student-friendly manner. With a blend of conceptual learning and problem-solving approach, it offers in-depth understanding of the basic mathematical and statistical tools. #introductiontostatistics

.jpg)

Chapter X of Companies Act 2013

Chapter X of Companies Act 2013 The company shall place the matter relating to such appointment for ratification by members at every annual general meeting. ... Under the Act, the provisions for rotation of auditors in the listed Company & certain other class of Companies, have been provided for. #chapterxofcompaniesact2013

.jpg)

Relevant sections under the Companies Act, 2013 dealing with fraud and false statements

Relevant sections under the Companies Act, 2013 dealing with fraud and false statements The new parent corporate law “The Companies Act 2013” is mostly ... I am limiting my write-up to the provisions to the Act, and I request the readers to refer relevant rules, if any, before ... in the 2013 Act is the Section 447 dealing with “Punishment for fraud”. ... Section 448

.jpg)

What is Corporate Image

What is Corporate Image A corporate identity or corporate image is the manner in which a corporation, firm or business enterprise presents itself to the public. The corporate identity is typically visualized by branding and with the use of trademarks, but it can also include things like product design, advertising, public relations etc #WhatisCorporateImage

.jpg)

What is Energy Audit

What is Energy Audit An energy audit is an inspection survey and an analysis of energy flows for energy conservation in a building. It may include a process or system to reduce the amount of energy input into the system without negatively affecting the output. #whatisenergyaudit